Trusted Worldwide Questions & Answers

Most Recent AICPA CPA-Financial Exam Dumps

Prepare for the AICPA CPA Financial Accounting and Reporting exam with our extensive collection of questions and answers. These practice Q&A are updated according to the latest syllabus, providing you with the tools needed to review and test your knowledge.

QA4Exam focus on the latest syllabus and exam objectives, our practice Q&A are designed to help you identify key topics and solidify your understanding. By focusing on the core curriculum, These Questions & Answers helps you cover all the essential topics, ensuring you're well-prepared for every section of the exam. Each question comes with a detailed explanation, offering valuable insights and helping you to learn from your mistakes. Whether you're looking to assess your progress or dive deeper into complex topics, our updated Q&A will provide the support you need to confidently approach the AICPA CPA-Financial exam and achieve success.

The questions for CPA-Financial were last updated on Apr 2, 2025.

- Viewing page 1 out of 33 pages.

- Viewing questions 1-5 out of 163 questions

In Yew Co.'s 1992 annual report, Yew described its social awareness expenditures during the year as follows:

"The Company contributed $250,000 in cash to youth and educational programs. The Company also gave $140,000 to health and human-service organizations, of which $80,000 was contributed by employees through payroll deductions. In addition, consistent with the Company's commitment to the environment, the Company spent $100,000 to redesign product packaging."

What amount of the above should be included in Yew's income statement as charitable contributions expense?

Choice 'a' is correct. Charitable contributions include amounts the company gave to recognized charities. This includes:

Note: Of the $140,000, employees gave $80,000, and the company $60,000. Redesigning packaging is not a contribution to a charity.

Choice 'b' is incorrect. The company gave only $60,000 of the $140,000. Employees gave $80,000.

Choice 'c' is incorrect. Redesigning packaging is not a contribution to a charity.

Choice 'd' is incorrect. The company gave only $60,000 of the $140,000. Employees gave $80,000.

Redesigning packaging is not a contribution to a charity.

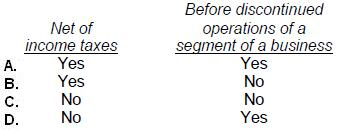

An extraordinary item should be reported separately on the income statement as a component of income:

Choice 'b' is correct, Yes - No. An extraordinary item should be reported separately on the income statement as a component of income:

Yes - net of income taxes.

No - after (not before) 'discontinued operations of a segment of a business.'

According to the FASB conceptual framework, which of the following statements conforms to the realization concept?

Choice 'b' is correct. Revenues and gains are realized when assets are exchanged for cash or claims to cash. SFAC 5 para. 83.

Choice 'a' is incorrect. Assigning depreciation in a production department is an example of allocating overhead. There is no realization associated with the assignment.

Choice 'c' is incorrect. The realization concept is integral to accounting for revenues and expenses and is not connected to collection of receivables.

Choice 'd' is incorrect. Assignment of overhead costs to products and thus to cost of goods sold is an example of matching. There is no realization associated with this assignment.

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before, and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List B represents the general accounting treatment required for these transactions. These treatments are:

* Cumulative effect approach - Include the cumulative effect of the adjustment resulting from the accounting change or error correction in the 1993 financial statements, and do not restate the 1992 financial statements.

* Retroactive or retrospective restatement approach - Restate the 1992 financial statements and adjust 1992 beginning retained earnings if the error or change affects a period prior to 1992.

* Prospective approach - Report 1993 and future financial statements on the new basis but do not restate 1992 financial statements.

During 1993, Quo increased its investment in Worth, Inc. from a 10% interest, purchased in 1992, to 30%, and acquired a seat on Worth's board of directors. As a result of its increased investment, Quo changed its method of accounting for investment in Worth, Inc. from the cost method to the equity method.

List B

Choice 'B' is correct. The equity method of accounting is applied retroactively when the investor has acquired 20% ownership. Prior to acquiring the ability to influence the investee, the cost method is proper. The retroactive restatement approach does not mean that this change is the correction of an error (which is now treated retroactively), a change in accounting principle (which is now treated retrospectively), or a change in accounting entity (which is now treated retrospectively). It just means that retroactive restatement is the proper treatment.

Goddard has used the FIFO method of inventory valuation since it began operations in 1987. Goddard decided to change to the weighted-average method for determining inventory costs at the beginning of 1990. The following schedule shows year-end inventory balances under the FIFO and weighted-average methods:

What amount, before income taxes, should be reported in the 1990 retained earnings statement as the cumulative effect of the change in accounting principle?

Choice 'a' is correct. $5,000 decrease.

The cumulative effect of change in accounting principle is determined as of the beginning of the year of change if comparative financial statements are not presented. In this case, the year of change is 1990, so the cumulative effect is the difference in inventory as of the end of 1989. [Note that inventory is a balance sheet item, so the change is based on the balances at the end of the last year the prior method was used. Had this question shown annual income statement amounts of cost of goods sold, we would have had to look at all the past years in the aggregate.] This will allow us to arrive at the adjustment to obtain the amount of retained earnings that would have been reported at the beginning of the period of change if the new accounting principle had been used for all prior periods.

Unlock All Questions for AICPA CPA-Financial Exam

Full Exam Access, Actual Exam Questions, Validated Answers, Anytime Anywhere, No Download Limits, No Practice Limits

Get All 163 Questions & Answers